Few entries on a credit report cause as much concern as a County Court Judgment (CCJ) or a default. These negative markers can affect your ability to obtain mortgages, loans, credit cards, car finance, mobile contracts, and even some tenancy agreements.

For many people, seeing a CCJ or default on their credit report can feel overwhelming. However, understanding how these markers work is the first step towards rebuilding your financial position.

The reality is that thousands of people across the UK successfully recover from CCJs and defaults every year. While these entries can create challenges, they do not necessarily prevent you from obtaining credit forever.

This guide explains what CCJs and defaults are, how they arise, how lenders view them, and what practical steps you can take to recover and improve your credit profile.

What Is a Default?

A default occurs when a lender believes a credit agreement has broken down due to missed payments.

Before a default is registered, a borrower will usually have fallen behind on payments for a significant period.

Defaults can occur on:

- Credit cards

- Personal loans

- Store cards

- Mobile phone contracts

- Utility accounts

- Finance agreements

A default signals to future lenders that the original agreement was not maintained according to its terms.

What Is a County Court Judgment (CCJ)?

A County Court Judgment is a court order issued in England, Wales, and Northern Ireland when a creditor successfully takes legal action to recover unpaid debt.

Typically, the process follows several stages:

- Missed payments occur

- The creditor contacts the borrower

- Collection efforts continue

- Court proceedings begin

- Judgment may be issued

A CCJ formally confirms that money is owed.

Unlike a default, a CCJ involves legal action through the courts.

CCJs vs Defaults: What’s the Difference?

Many people assume they are the same.

They are not.

Default

A lender’s decision that an account has broken down.

CCJ

A court’s decision that money is owed.

It is possible to have:

- A default without a CCJ

- A CCJ following a default

- Multiple defaults

- Multiple CCJs

Generally speaking, CCJs are often viewed as more serious because they involve legal proceedings.

Common Reasons People Receive Defaults

Most defaults result from ongoing repayment difficulties.

Common causes include:

Financial Hardship

Unexpected financial pressures may make repayments difficult.

Job Loss

Income reductions can affect affordability.

Illness

Health issues can disrupt financial stability.

Relationship Breakdown

Separation or divorce frequently creates financial strain.

Rising Living Costs

Higher household expenses can make debt harder to manage.

Poor Financial Planning

Overspending and excessive borrowing can eventually lead to missed payments.

Defaults are often symptoms of wider financial difficulties rather than isolated events.

Common Reasons People Receive CCJs

CCJs typically occur when debts remain unresolved.

Common situations include:

Ignoring Debt Collection Letters

Some people avoid communication due to anxiety or uncertainty.

Disputed Debts

Disagreements sometimes escalate into legal action.

Unpaid Loans

Persistent non-payment may result in court proceedings.

Utility Debt

Unpaid utility bills can occasionally lead to legal action.

Old Addresses

Some individuals are unaware of proceedings because correspondence was sent elsewhere.

Ignoring court documents is one of the biggest mistakes borrowers can make.

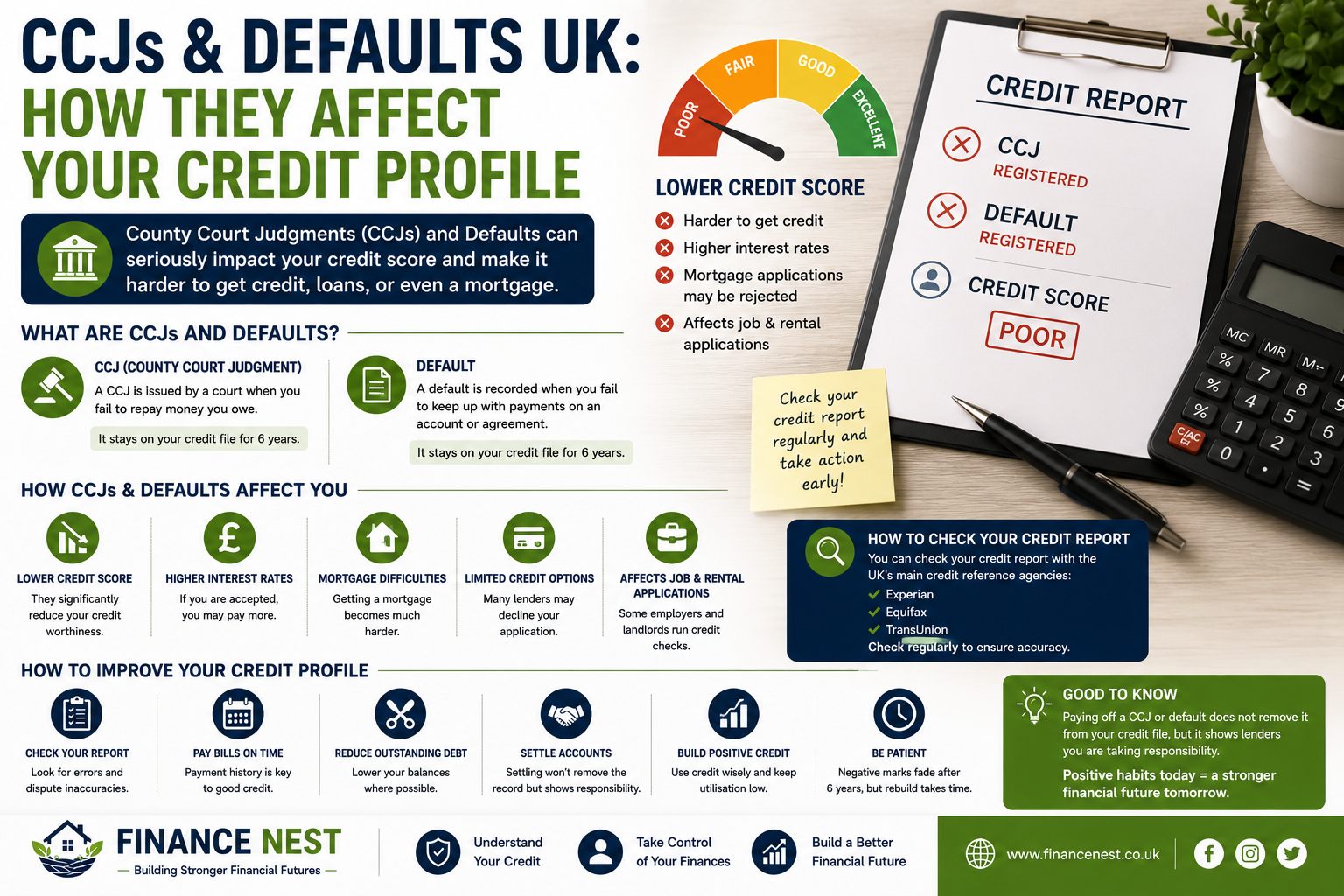

How CCJs and Defaults Affect Credit Reports

Both entries can significantly impact creditworthiness.

Lenders often view them as indicators of previous financial difficulties.

Potential effects include:

- Reduced approval chances

- Higher interest rates

- Lower credit limits

- Additional lender scrutiny

- Restricted borrowing options

The severity of the impact depends on:

- Age of the entry

- Amount involved

- Number of entries

- Whether debts have been settled

- Overall credit profile

How Lenders Assess CCJs and Defaults

Not all lenders evaluate credit issues identically.

Some lenders focus heavily on:

Recency

Recent problems are often viewed more seriously.

Frequency

Multiple issues may indicate ongoing financial difficulties.

Severity

Large unpaid debts may raise greater concerns.

Resolution

Settled debts often appear more favourable than unresolved debts.

Overall Circumstances

Income and affordability still matter.

A person with a historic default and strong current finances may be viewed differently from someone experiencing ongoing financial difficulties.

Can You Get a Mortgage with a CCJ?

Yes, although options may be more limited.

Mortgage lenders generally consider:

When the CCJ Occurred

Older CCJs are often viewed more favourably.

Whether It Has Been Satisfied

Settled judgments may improve lender confidence.

Deposit Size

Larger deposits can strengthen applications.

Current Financial Stability

Stable income and responsible recent behaviour are important.

Number of CCJs

Multiple judgments may increase complexity.

Some specialist lenders specifically assist borrowers with historic credit issues.

Can You Get a Loan with a Default?

Possibly.

The outcome depends on:

- Lender criteria

- Severity of the default

- Current financial circumstances

- Affordability assessment

Borrowers with defaults may sometimes face:

- Higher interest rates

- Lower borrowing limits

- Fewer lender options

Comparing products carefully is essential.

What Does “Satisfied” Mean?

A CCJ or default may be marked as satisfied when the outstanding debt has been repaid.

While satisfaction does not erase the record immediately, it can demonstrate responsibility and willingness to resolve financial obligations.

Many lenders view settled debts more positively than unresolved debts.

If you repay a debt, ensure records are updated correctly.

Should You Pay an Old Default?

In many cases, resolving debts can be beneficial.

Potential advantages include:

- Reduced collection activity

- Improved financial organisation

- Better lender perception

However, every situation differs.

Large debts, disputed debts, or legal matters may require professional advice.

Rebuilding After a Default

Recovery begins with consistent positive behaviour.

Step 1: Review Your Credit Reports

Check all major agencies:

- Experian

- Equifax

- TransUnion

Confirm information is accurate.

Step 2: Correct Errors

Incorrect entries should be challenged promptly.

Examples include:

- Wrong balances

- Incorrect dates

- Duplicate records

Step 3: Create a Budget

A realistic budget helps prevent future repayment problems.

Focus on:

- Essential spending

- Debt repayments

- Savings contributions

Step 4: Maintain Perfect Payment History

Future payment behaviour matters.

Consistent on-time payments gradually strengthen lender confidence.

Step 5: Reduce Existing Debt

Lower debt levels often improve affordability and financial stability.

Step 6: Build Emergency Savings

Emergency funds can reduce reliance on borrowing during unexpected situations.

Mistakes to Avoid

Ignoring Credit Problems

Avoidance often increases costs and stress.

Applying Repeatedly for Credit

Multiple applications may worsen approval chances.

Falling for Credit Repair Scams

No company can legally remove accurate information from your credit file simply because you pay a fee.

Missing New Payments

Recent missed payments can delay recovery significantly.

Ignoring Court Documents

Always respond to court correspondence promptly.

How Long Do CCJs and Defaults Matter?

The influence of negative entries generally decreases over time.

Lenders often place greater emphasis on:

- Recent payment behaviour

- Current debt levels

- Affordability

- Financial stability

The key message is simple:

A historic problem combined with strong recent financial behaviour is usually viewed more positively than ongoing difficulties.

Frequently Asked Questions

Is a CCJ worse than a default?

Many lenders consider a CCJ more serious because it involves court action.

Can a CCJ be removed?

Accurate CCJs generally remain according to reporting rules unless successfully challenged through appropriate legal procedures.

Will paying a default improve my credit profile?

Settling debts can demonstrate responsibility and may improve lender perception.

Can I get a mortgage after a CCJ?

Possibly. Many lenders consider applications individually.

Should I use a credit repair company?

Be cautious. Accurate information generally cannot be removed simply by paying a third party.

Final Thoughts

CCJs and defaults are serious credit events, but they do not have to define your financial future.

Many people experience financial setbacks due to circumstances beyond their control. What matters most is how you respond.

By understanding your credit reports, resolving outstanding issues, maintaining perfect payment habits, reducing debt and building financial resilience, you can gradually rebuild lender confidence and strengthen your financial profile.

Recovery takes time, but consistent positive action can create significant improvements and open new opportunities for borrowing, home ownership and long-term financial security.

Disclaimer: This article is for educational purposes only and does not constitute legal, debt, mortgage or financial advice. If you are experiencing debt difficulties or legal proceedings, consider seeking advice from a qualified professional or recognised debt charity.