A household budget helps you understand where money comes from, where it goes and what needs to change. It is not about restricting every purchase. A good budget gives you control, reduces surprises and helps you plan for bills, savings, debt repayments and everyday spending.

What is a household budget?

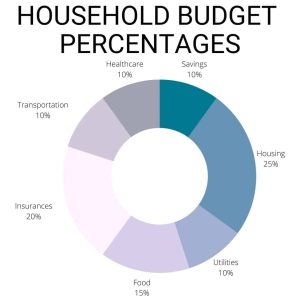

A household budget is a plan for income and spending over a set period, usually a month. It can cover one person, a couple, a family or a shared household. The budget should reflect real life, including irregular costs that do not happen every month.

The best budget is one you can actually use. A complicated spreadsheet is not helpful if you never update it.

Start with income

List all regular income after tax, including wages, self-employed drawings, benefits, pensions, maintenance payments or rental income. If income varies, use a conservative average or base your budget on the lowest typical month.

Variable-income households may benefit from building a buffer account to smooth out good and bad months.

List fixed bills

Fixed bills are payments that happen regularly and are relatively predictable. These may include rent or mortgage, council tax, utilities, broadband, mobile phone, insurance, childcare, loan repayments and subscriptions.

Check whether bills are monthly, quarterly or annual. Annual costs should be divided by twelve and saved monthly into a separate pot.

Track flexible spending

Flexible spending includes food, fuel, transport, clothing, entertainment, takeaways, gifts and personal spending. This is where many budgets fail because people underestimate normal daily purchases.

Review bank statements and card transactions rather than guessing. A realistic budget is more useful than an optimistic one.

Plan for irregular costs

Irregular costs can damage a budget if they are ignored. Examples include car repairs, school uniforms, Christmas, birthdays, holidays, dental costs, home maintenance and insurance renewals.

Create sinking funds for predictable annual or occasional costs. This means saving a small amount each month so the money is ready when needed.

Popular budgeting methods

- Zero-based budgeting: Give every pound a job so income minus spending, saving and debt repayments equals zero.

- 50/30/20 method: Split income between needs, wants and savings or debt repayment.

- Envelope or pot system: Separate money into categories to avoid overspending.

- Pay-yourself-first: Save immediately after payday before spending begins.

Budgeting as a couple or family

Joint budgeting requires communication. Decide which bills are shared, how contributions are calculated and how personal spending is handled. Some couples split costs equally, while others split proportionally based on income.

Avoid using a budget as a blame tool. The aim is teamwork and clarity.

How to review your budget

- Compare planned spending with actual spending.

- Identify categories that were unrealistic.

- Adjust for upcoming events.

- Move unused money to savings or debt repayment.

- Review bills before renewal dates.

- Set one improvement goal for the next month.

Frequently asked questions

How often should I update my budget?

Monthly works for most households, but weekly check-ins can help if money is tight.

What if my income changes every month?

Use a conservative income estimate and build a buffer during stronger months.

Should children be included in budgeting?

Age-appropriate conversations can help children understand saving, bills and choices.

What is the biggest budgeting mistake?

Ignoring irregular costs is one of the most common reasons budgets fail.

Final thoughts

A household budget should reduce stress, not create it. Keep it simple, update it regularly and build in room for real life.

Disclaimer: This article is for general information only and does not constitute financial advice. Seek professional support if debt or bills are becoming unmanageable.