Many people focus on their credit score without understanding the factors that influence it. One of the most important is credit utilisation, a term used to describe how much of your available revolving credit you are currently using.

Although it sounds technical, credit utilisation is actually quite simple. If you have a credit card with a £2,000 limit and a balance of £1,000, your utilisation is 50%. If you owe only £200, your utilisation is 10%.

Lenders often look beyond whether you make payments on time. They also consider how heavily you rely on available credit. A person who consistently uses nearly all of their available credit may appear riskier than someone who uses a smaller proportion and manages repayments comfortably.

Understanding credit utilisation can help improve your credit profile, increase approval chances for future borrowing, and potentially access better interest rates.

What Is Credit Utilisation?

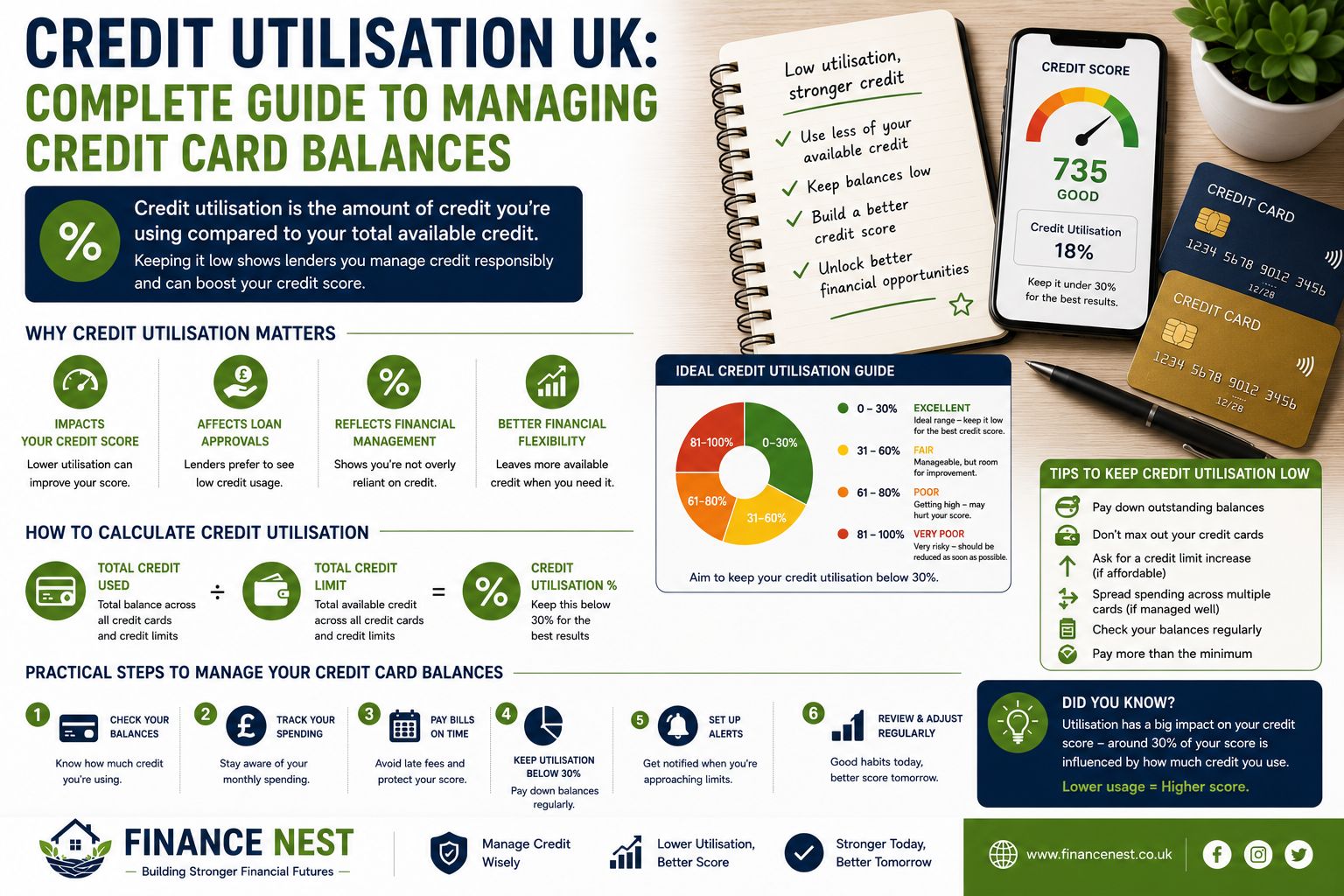

Credit utilisation measures the relationship between your outstanding balances and your available credit limits.

The formula is:

Credit Utilisation = Outstanding Balance ÷ Credit Limit × 100

For example:

| Credit Limit | Balance | Utilisation |

|---|---|---|

| £1,000 | £100 | 10% |

| £2,000 | £1,000 | 50% |

| £5,000 | £4,500 | 90% |

The percentage can be calculated for an individual credit card or across all revolving credit accounts.

Most credit reference agencies and lenders view lower utilisation more favourably than very high utilisation.

Why Lenders Care About Credit Utilisation

When lenders assess applications, they try to understand risk.

A customer using most of their available credit every month may be perceived as more financially stretched than someone with lower balances.

High utilisation may suggest:

- Heavy dependence on borrowing

- Limited financial flexibility

- Increased likelihood of repayment difficulties

- Potential cash-flow challenges

Low utilisation can indicate:

- Responsible borrowing habits

- Financial stability

- Better money management

- Lower borrowing risk

Credit utilisation is only one factor among many, but it can play a significant role in lending decisions.

Does Credit Utilisation Affect Credit Scores?

Although each credit reference agency uses different scoring models, utilisation commonly contributes to credit assessment calculations.

A person with excellent payment history but consistently high credit utilisation may not achieve the strongest possible credit profile.

Similarly, reducing utilisation often leads to improvements in credit indicators over time.

However, no single percentage guarantees approval or rejection. Lenders also consider:

- Income

- Employment stability

- Existing debts

- Payment history

- Electoral roll registration

- Previous defaults or CCJs

- Affordability assessments

Credit utilisation should therefore be viewed as one part of a broader financial picture.

Understanding Overall vs Individual Utilisation

Many consumers only consider total utilisation.

However, lenders may review both:

Overall Utilisation

This measures balances across all revolving credit accounts.

Example:

| Card | Limit | Balance |

|---|---|---|

| Card A | £2,000 | £500 |

| Card B | £3,000 | £500 |

Total limit: £5,000

Total balance: £1,000

Overall utilisation: 20%

Individual Utilisation

Each card may also be considered separately.

For example:

| Card | Utilisation |

|---|---|

| Card A | 25% |

| Card B | 17% |

Both appear manageable.

Now consider:

| Card | Limit | Balance |

|---|---|---|

| Card A | £1,000 | £950 |

| Card B | £4,000 | £50 |

Overall utilisation remains 20%.

However, Card A is almost maxed out.

Some lenders may still view this negatively.

What Is Considered Good Credit Utilisation?

There is no official UK rule.

However, many financial professionals suggest:

Under 30%

Generally considered healthy.

Under 20%

Often viewed positively.

Under 10%

Typically regarded as excellent management.

Above 75%

May raise concerns with some lenders.

Near 100%

Often suggests significant reliance on available credit.

Remember that every lender uses different criteria.

Common Reasons Credit Utilisation Increases

Many people unintentionally increase utilisation.

Common causes include:

Large One-Off Purchases

Home appliances, holidays or emergency repairs can temporarily raise balances.

Reduced Income

Unexpected financial pressures may increase reliance on credit cards.

Interest Charges

Existing balances can grow if repayments only cover minimum amounts.

Multiple Small Purchases

Regular spending can accumulate faster than expected.

Poor Budgeting

Lack of spending oversight frequently leads to higher balances.

Practical Ways to Lower Credit Utilisation

Make Additional Payments

Instead of waiting until the monthly due date, consider making smaller payments throughout the month.

This can reduce balances before reporting dates.

Increase Repayments

Paying more than the minimum reduces balances faster and limits interest costs.

Create a Spending Plan

Budgeting helps prevent unnecessary credit usage.

Track:

- Groceries

- Transport

- Entertainment

- Subscriptions

- Household costs

Use Debit Instead of Credit

Where possible, use available cash rather than borrowing.

Avoid Unnecessary Purchases

Small discretionary spending can quickly increase balances.

Should You Increase Your Credit Limit?

Some consumers receive offers to increase credit limits.

This can reduce utilisation percentages if spending remains unchanged.

Example:

Balance: £1,000

Current limit: £2,000

Utilisation: 50%

New limit: £4,000

Utilisation: 25%

However, increased limits only help if spending remains controlled.

For some individuals, larger limits create temptation to borrow more.

Always consider personal spending habits before accepting higher limits.

Balance Transfers and Credit Utilisation

Balance transfers may help manage utilisation and interest costs.

Benefits can include:

- Lower promotional interest rates

- Simpler debt management

- Reduced monthly interest

However:

- Transfer fees may apply

- Promotional periods eventually end

- New spending can create additional debt

Balance transfers should support repayment plans rather than delay them.

Credit Utilisation and Mortgage Applications

Mortgage lenders assess affordability carefully.

High utilisation can sometimes:

- Reduce borrowing potential

- Trigger additional scrutiny

- Affect lender confidence

Before applying for a mortgage:

- Review all credit reports

- Reduce unnecessary balances

- Avoid major new borrowing

- Correct any reporting errors

Many mortgage advisers recommend preparing credit profiles months before applying.

Common Myths About Credit Utilisation

Myth 1: Never Use Credit Cards

False.

Responsible use can demonstrate account management.

Myth 2: Higher Limits Always Mean Better Credit

Not necessarily.

Higher limits only help if balances remain manageable.

Myth 3: Paying Minimum Payments Is Enough

Minimum payments keep accounts current but often prolong debt repayment.

Myth 4: Utilisation Doesn’t Matter

Many lenders consider utilisation as part of overall risk assessment.

Frequently Asked Questions

Does checking my utilisation affect my credit score?

No. Reviewing your own accounts does not usually impact your credit profile.

Is 0% utilisation best?

Not always. Some account activity combined with responsible repayment can demonstrate active credit management.

Should I close unused credit cards?

Not automatically. Closing cards reduces available credit and may increase utilisation percentages.

How quickly can utilisation improve?

Changes may appear after updated balances are reported by lenders.

Does utilisation matter for all credit products?

It is most relevant for revolving credit such as credit cards and overdrafts.

Final Thoughts

Credit utilisation is one of the easiest aspects of a credit profile to understand and improve. While it is not the only factor lenders consider, managing balances carefully can strengthen your overall financial position.

Reducing reliance on available credit, maintaining a realistic budget, paying more than minimum payments and regularly reviewing accounts can all contribute to healthier borrowing habits.

Over time, these actions may improve how lenders view your credit profile and support future financial goals.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always consider your personal circumstances before making financial decisions.