Life has a habit of throwing unexpected financial challenges our way. A boiler breaks down in the middle of winter, the car fails its MOT, a pet needs emergency treatment, or an unexpected redundancy affects household income. While many people focus on earning more money or investing for the future, one of the most important foundations of financial security is often overlooked: the emergency fund.

An emergency fund is money set aside specifically for unexpected expenses or periods of financial hardship. It acts as a financial safety net, helping you deal with life’s surprises without relying on credit cards, loans, or overdrafts.

In recent years, rising living costs, inflation, and economic uncertainty have highlighted the importance of having accessible savings. Many UK households live from payday to payday, leaving little room to absorb financial shocks. An emergency fund can provide peace of mind, reduce stress, and help prevent short-term problems from becoming long-term debt.

This guide explains what an emergency fund is, how much you should save, where to keep your savings, and practical strategies to build your financial safety net.

What Is an Emergency Fund?

An emergency fund is a dedicated savings pot designed exclusively for unexpected financial emergencies.

It is not:

- A holiday fund

- Christmas savings

- A house deposit

- Investment money

- Spending money for planned purchases

Instead, it is money reserved for genuine emergencies that could otherwise cause financial hardship.

Examples include:

- Emergency home repairs

- Boiler replacement

- Essential car repairs

- Unexpected veterinary bills

- Medical expenses

- Sudden loss of income

- Family emergencies

- Urgent travel costs

The primary purpose of an emergency fund is to protect your financial stability when something unexpected happens.

Why Is an Emergency Fund Important?

Many people underestimate how quickly a financial emergency can escalate.

Without savings, unexpected costs often lead to:

- Credit card debt

- Personal loans

- Payday borrowing

- Overdraft usage

- Missed bills

- Financial stress

An emergency fund helps break this cycle.

Financial Protection

Unexpected expenses become manageable when funds are already available.

Reduced Stress

Knowing you have savings available provides confidence and peace of mind.

Less Reliance on Debt

You are less likely to borrow at high interest rates.

Greater Financial Flexibility

Emergency savings provide options during difficult periods.

Improved Financial Stability

Households with emergency funds are generally better positioned to handle financial shocks.

What Qualifies as a Financial Emergency?

One of the most common mistakes is using emergency savings for non-emergency spending.

A useful question to ask is:

Was this expense unexpected, necessary, and urgent?

If the answer is yes, it may qualify as an emergency.

Examples of Genuine Emergencies

- Boiler failure

- Car breakdown

- Redundancy

- Urgent dental treatment

- Major home repairs

- Essential appliance replacement

- Emergency travel

Examples That Are Not Emergencies

- Holidays

- Christmas spending

- New gadgets

- Planned home improvements

- Designer clothing

- Dining out

Separating wants from genuine emergencies helps preserve the purpose of the fund.

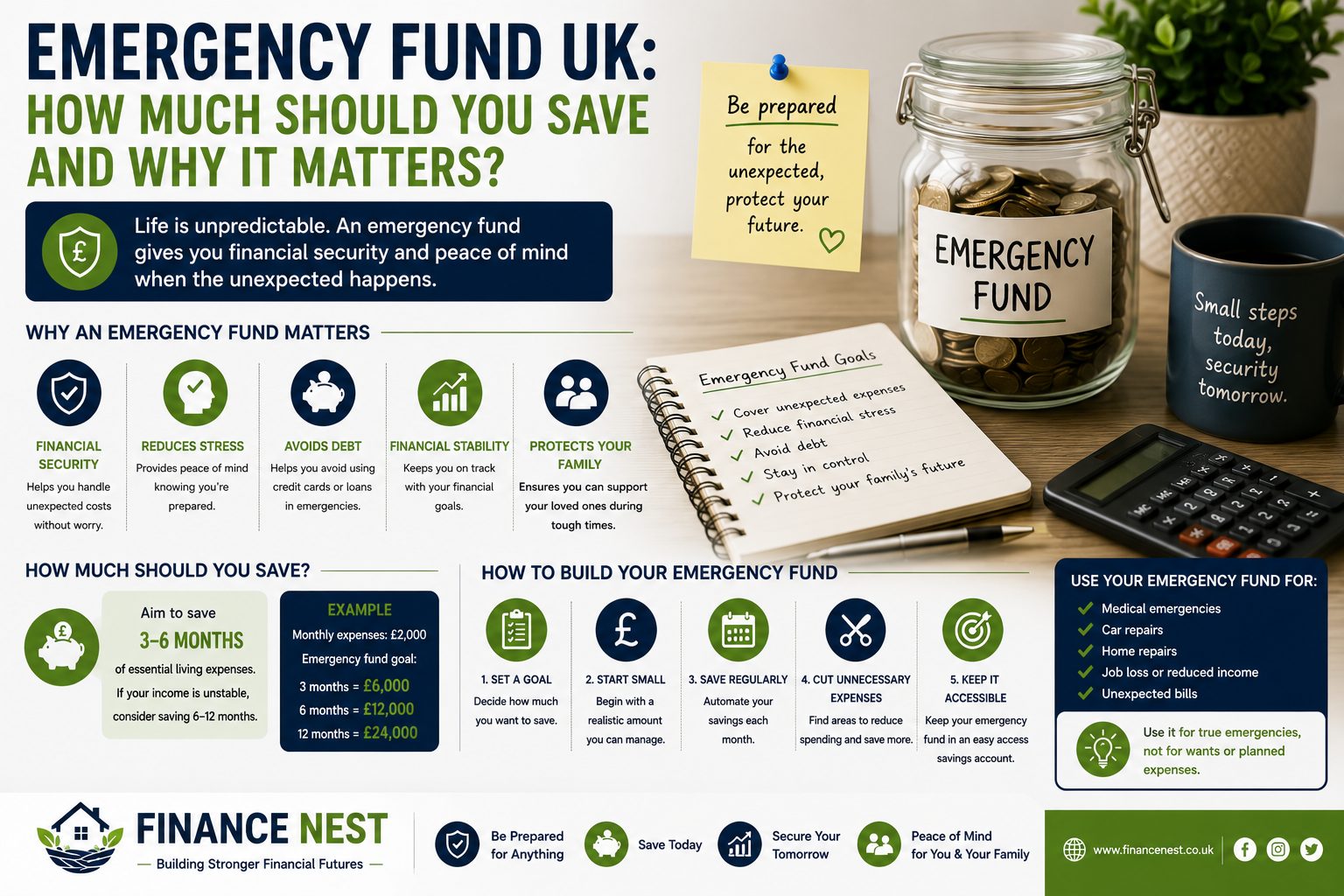

How Much Should You Save?

There is no universal answer.

The ideal emergency fund depends on:

- Income stability

- Family size

- Housing costs

- Existing debt

- Employment situation

- Monthly expenses

Financial experts often recommend saving between three and six months of essential living expenses.

Three-Month Emergency Fund

Suitable for many people with:

- Stable employment

- Multiple household incomes

- Low debt levels

Example:

Monthly essential expenses: £1,500

Emergency fund target:

£1,500 × 3 = £4,500

Six-Month Emergency Fund

Often recommended for:

- Self-employed workers

- Single-income households

- Freelancers

- Individuals with irregular income

Example:

Monthly essential expenses: £2,000

Emergency fund target:

£2,000 × 6 = £12,000

Start Smaller if Necessary

Many people become discouraged by large targets.

Instead, focus on milestones.

Stage One

Save £500

Stage Two

Save £1,000

Stage Three

Save one month of expenses

Stage Four

Save three months

Stage Five

Build towards six months

Progress is more important than perfection.

Calculating Your Essential Expenses

Your emergency fund should cover necessities rather than your full lifestyle.

Essential expenses typically include:

- Rent or mortgage

- Council tax

- Utilities

- Food

- Insurance

- Transport

- Childcare

- Minimum debt payments

- Internet and phone bills

Optional spending generally includes:

- Holidays

- Entertainment

- Dining out

- Subscriptions

- Luxury purchases

Calculating your true essentials provides a realistic savings target.

Where Should You Keep Your Emergency Fund?

Accessibility is one of the most important factors.

Your emergency fund should be:

- Safe

- Accessible

- Easy to manage

Easy Access Savings Accounts

Many people choose easy-access savings accounts.

Advantages:

- Quick access to funds

- Interest earnings

- Separation from everyday spending

Potential disadvantages:

- Lower interest rates than some fixed products

Cash ISAs

Some savers prefer Cash ISAs because interest may be tax-efficient depending on individual circumstances.

Benefits include:

- Easy access options available

- Potential tax advantages

Premium Bonds

Some UK savers use Premium Bonds.

Advantages:

- Government-backed

- Potential prize draws

Disadvantages:

- No guaranteed return

Avoid Risky Investments

Emergency savings generally should not be invested in:

- Individual shares

- Cryptocurrencies

- High-risk investments

The value of investments can fall at the exact moment you need access to your money.

The priority of an emergency fund is security, not growth.

Emergency Fund vs Paying Off Debt

This is one of the most common personal finance questions.

Should you save or repay debt first?

The answer depends on your situation.

High-Interest Debt

If you have expensive borrowing such as credit cards, balancing debt repayment and savings becomes important.

A small starter emergency fund can prevent further borrowing when unexpected expenses arise.

Many people aim to:

- Build a starter emergency fund

- Focus on high-interest debt

- Expand emergency savings later

Low-Interest Debt

For lower-cost borrowing, building emergency savings may become a higher priority.

Every financial situation is different.

How to Build an Emergency Fund

Building savings can feel difficult, especially during periods of rising living costs.

However, consistent small contributions can produce significant results.

Automate Your Savings

One of the most effective strategies is automation.

Arrange a transfer immediately after payday.

Even:

- £20 per week

- £50 per month

- £100 per month

can grow steadily over time.

Save Windfalls

Unexpected money can accelerate progress.

Examples include:

- Tax refunds

- Bonuses

- Cashback rewards

- Gifts

- Overtime payments

Saving a portion of windfalls can quickly increase balances.

Reduce One Expense

Small changes can create long-term savings.

Examples:

- Cancel unused subscriptions

- Reduce takeaway spending

- Compare insurance policies

- Switch utility providers

Redirect savings into your emergency fund.

Use a Separate Account

Keeping emergency savings separate reduces temptation.

Many people find it easier to leave savings untouched when they are not visible in their everyday banking balance.

Common Emergency Fund Mistakes

Waiting Until You Can Save Large Amounts

Small contributions are better than no contributions.

Using Savings for Non-Emergencies

This undermines the purpose of the fund.

Keeping Savings in a Current Account

Easy access can increase unnecessary spending.

Ignoring Inflation

Review your target periodically to ensure it remains appropriate.

Never Replenishing the Fund

If you use emergency savings, rebuild them as soon as possible.

Emergency Funds for Different Life Stages

Young Professionals

Focus on creating the habit of saving regularly.

Families

Larger households often face more potential unexpected expenses.

A larger emergency fund may provide additional security.

Homeowners

Home ownership can involve expensive repairs.

Emergency savings become particularly important.

Self-Employed Workers

Income fluctuations often make larger emergency funds beneficial.

Frequently Asked Questions

Is £1,000 enough for an emergency fund?

It is an excellent starting point but may not cover larger emergencies or extended income loss.

Should I invest my emergency fund?

Emergency savings are generally best kept in low-risk, accessible accounts.

Can I use a credit card instead?

Credit cards provide borrowing, not savings. They can increase financial pressure if repayments become difficult.

How long does it take to build an emergency fund?

This depends on your target and monthly savings contributions. Consistency matters more than speed.

Should couples have a joint emergency fund?

Many couples choose to maintain shared emergency savings, although individual circumstances vary.

Final Thoughts

An emergency fund is one of the most powerful tools for improving financial security. While investing, mortgage planning, and retirement savings often attract attention, emergency savings form the foundation that supports every other financial goal.

Unexpected events are part of life. While you cannot always predict when they will occur, you can prepare for them.

Start with a realistic target, save consistently, and focus on building a financial cushion that protects you and your family from unnecessary stress and debt.

Over time, even modest contributions can grow into a valuable safety net that provides confidence, stability, and peace of mind.

Disclaimer: This article is for general educational purposes only and does not constitute financial advice. Always consider your individual circumstances and seek professional advice where appropriate.