Ask most people why they struggle with money, and you’ll often hear the same response:

“I don’t know where my money goes each month.”

This is exactly where budgeting can help.

Despite what many people think, budgeting is not about depriving yourself of everything you enjoy. It is not about living on the bare minimum or tracking every penny with military precision. Instead, a budget is simply a plan for your money.

A good budget helps you:

- Understand your spending habits

- Avoid running out of money before payday

- Build savings

- Reduce debt

- Achieve financial goals

- Feel more in control of your finances

The problem is that many budgets fail because they are unrealistic. People often create strict plans that look good on paper but are impossible to maintain in real life.

The goal is not to create a perfect budget.

The goal is to create a budget that actually works for your lifestyle.

What Is a Budget?

A budget is a financial plan that outlines:

- How much money you earn

- How much money you spend

- Where your money goes

- How much you save

Think of a budget as a roadmap.

Without a roadmap, it’s easy to get lost financially.

With a budget, every pound has a purpose.

Why Most Budgets Fail

Before creating a successful budget, it’s important to understand why many people give up.

Unrealistic Expectations

Many budgets fail because they cut spending too aggressively.

For example:

- Eliminating all entertainment

- Cutting food spending too far

- Removing every luxury

While this may work for a few weeks, it often becomes unsustainable.

Not Tracking Spending

Creating a budget is only the first step.

Without monitoring spending, it’s impossible to know whether you’re following the plan.

Forgetting Irregular Expenses

Many people budget for monthly bills but forget annual or seasonal expenses such as:

- Car servicing

- Christmas

- School uniforms

- Insurance renewals

- Holidays

These costs eventually appear and disrupt the budget.

Giving Up After One Mistake

A single overspending month does not mean the budget has failed.

Successful budgeting is about consistency, not perfection.

Step 1: Calculate Your Income

The first stage is understanding how much money comes into your household.

Include:

Employment Income

- Salary

- Wages

- Bonuses

Self-Employment Income

- Business earnings

- Freelance income

Benefits

- Child Benefit

- Universal Credit

- Other support payments

Other Sources

- Rental income

- Pension income

- Side hustle earnings

Use your net income after tax and deductions.

This represents the actual money available for spending and saving.

Step 2: Track Your Current Spending

Before creating a budget, understand your current habits.

Review:

- Bank statements

- Credit card statements

- Digital wallet transactions

Look at the previous three months if possible.

Most people discover spending patterns they had not noticed before.

Categorise Your Spending

Divide expenses into categories.

Housing

- Mortgage

- Rent

- Service charges

Utilities

- Gas

- Electricity

- Water

- Broadband

Food

- Groceries

- Household items

Transport

- Fuel

- Public transport

- Vehicle maintenance

Insurance

- Home insurance

- Car insurance

- Life insurance

Entertainment

- Streaming services

- Hobbies

- Social activities

Savings

- Emergency fund

- Investments

- Goal-based savings

Categorising spending makes it easier to identify areas for improvement.

Step 3: Identify Fixed and Variable Expenses

Not all spending behaves the same way.

Fixed Expenses

These remain relatively stable.

Examples:

- Rent

- Mortgage

- Insurance

- Mobile contracts

Variable Expenses

These change from month to month.

Examples:

- Food

- Fuel

- Entertainment

- Clothing

Variable expenses often provide the greatest opportunities for savings.

Step 4: Set Financial Goals

A budget without goals can feel pointless.

Goals provide motivation.

Examples include:

Short-Term Goals

- Save £1,000 emergency fund

- Clear credit card debt

- Pay for a holiday

Medium-Term Goals

- Save for a house deposit

- Buy a vehicle

Long-Term Goals

- Retirement planning

- Investment growth

- Financial independence

The clearer the goal, the easier it becomes to stay committed.

Popular Budgeting Methods

Different approaches suit different personalities.

The 50/30/20 Rule

One of the simplest budgeting methods.

Allocate:

50% Needs

- Housing

- Utilities

- Food

- Transport

30% Wants

- Entertainment

- Dining out

- Hobbies

20% Savings and Debt Repayment

- Emergency fund

- Investments

- Additional debt payments

This method provides flexibility while encouraging financial discipline.

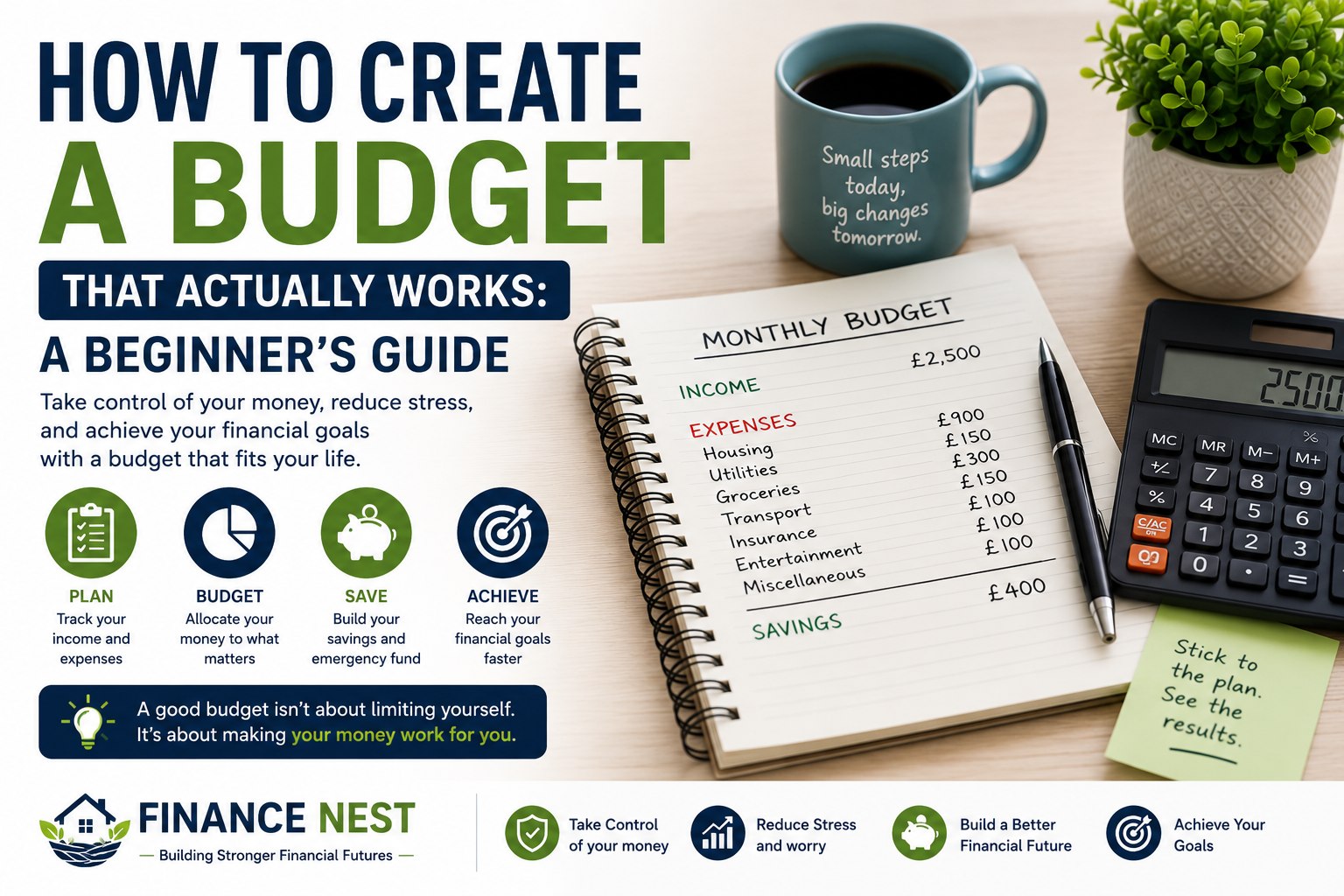

Zero-Based Budgeting

With this method, every pound receives a purpose.

Income minus expenses equals zero.

For example:

Income: £2,500

Expenses:

- Housing: £900

- Food: £300

- Savings: £300

- Transport: £200

- Other categories: £800

Remaining balance: £0

This does not mean spending everything.

It means assigning every pound intentionally.

Pay Yourself First

This approach prioritises savings before discretionary spending.

For example:

- Salary arrives

- Savings transferred automatically

- Remaining money used for expenses

Many successful savers use this strategy.

How to Build a Budget You Can Stick To

Be Realistic

A budget should reflect your actual life.

If you enjoy occasional meals out, include them.

Completely eliminating enjoyable spending often causes budgets to fail.

Include Fun Money

Giving yourself a small discretionary spending allowance can improve long-term success.

Plan for Unexpected Expenses

Life is unpredictable.

Include a small buffer category in your budget.

Review Monthly

Budgets are not static.

Income, expenses and priorities change over time.

Using Technology to Budget

Modern tools make budgeting easier.

Popular options include:

Banking Apps

Many banks categorise spending automatically.

Spreadsheet Templates

Ideal for detailed budgeting.

Budgeting Apps

Can provide insights and spending alerts.

Savings Apps

Help automate saving goals.

Choose a system that you find easy to maintain.

Budgeting as a Couple

Money is one of the most common sources of relationship tension.

Successful couples often:

- Share goals

- Communicate regularly

- Review finances together

- Agree spending priorities

Joint budgeting promotes transparency and teamwork.

Budgeting for Families

Families face unique financial challenges.

Common costs include:

- Childcare

- School expenses

- Activities

- Growing food bills

Family budgets should account for both predictable and unexpected expenses.

Meal planning, bulk purchasing and annual budgeting can be particularly helpful.

Common Budgeting Mistakes

Ignoring Small Purchases

Small daily expenses can become surprisingly expensive over a year.

Not Saving for Emergencies

Without savings, unexpected costs often lead to debt.

Relying on Credit

Using borrowing to fill budget gaps creates long-term problems.

Comparing Yourself to Others

Budgets should reflect your circumstances, not someone else’s lifestyle.

Expecting Instant Results

Financial improvement usually takes time.

Frequently Asked Questions

How much should I save each month?

There is no universal answer. The amount depends on your goals and financial circumstances.

What if my income changes every month?

Base your budget on average income and maintain a financial buffer where possible.

Should I use cash or cards?

Both can work. Choose whichever helps you control spending most effectively.

Is budgeting worth it if I have little money?

Yes. Budgeting is often most valuable when finances are tight.

How often should I review my budget?

Monthly reviews are generally recommended.

Final Thoughts

Creating a budget is one of the most important steps you can take towards financial stability.

A successful budget is not about restricting every aspect of your life. It is about making conscious decisions about where your money goes and ensuring it supports your goals and priorities.

Start simple, be realistic, and focus on progress rather than perfection.

The most effective budgets are not necessarily the most detailed. They are the ones that people consistently follow.

Over time, a well-managed budget can help you reduce stress, build savings, eliminate debt, and create a stronger financial future.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always consider your personal circumstances before making financial decisions.